January is often the point in the year when Self Assessment work comes to the forefront.

Returns need to be filed, and clients expect clear answers about what they owe and when. The work gets done, but the cost can be long days, pressure on the team and very little space for anything beyond compliance. The work gets done, but the cost can be long days, pressure on the team and very little space for anything beyond compliance.

When you look closely at what creates that pressure, it is rarely just the mechanics of submitting a return. It is a mix of the timing of conversations and whether the team has the right information from clients early enough to act on it.

This article looks at how a more deliberate approach to Self Assessment planning can make January feel calmer, without asking your team to redesign their year from scratch.

Why January feels so heavy

In a typical Self Assessment cycle, information and decisions accumulate over time.

Directors adjust drawings. Clients make pension contributions, take bonuses, start renting out property, start a side gig or change how they work. Notes sit in emails, working papers, meeting summaries and spreadsheets.

Most of this is manageable during the year. The strain appears when everything is pulled together for filing, often months after the decision was made.

The timing against the tax year and filing deadline matters as well. For example:

- Tax year ends: 5 April 2025

- Filing deadline for that year: 31 January 2026

Any decisions a client makes before 5 April 2025 will feed into the return due by 31 January 2026. Decisions made from 6 April 2025 onwards will not affect that return at all. They will not show up until the Self Assessment due by 31 January 2027.

By January, the team is frequently:

- Chasing missing information

- Piecing together what changed, and when

- Explaining tax payments that now feel fixed rather than flexible

HMRC statistics underline the scale of that peak. In the most recent Self Assessment cycle (2023–24), more than 11.5 million taxpayers filed by the 31 January 2025 deadline, with around 1.1 million still missing it and facing late-filing penalties.

The returns are submitted, but a lot of the thinking has been squeezed into the same narrow window. That is what makes January feel so heavy.

The real issue: when planning happens

Self Assessment is often treated as an annual event. Planning conversations are tied to the return, rather than to the year in which decisions are made.

A director draws more than usual. A client changes their pension contributions. Someone takes a bonus at year-end. Each decision may be reasonable at the time, but the full effect is only understood when the return is prepared.

At that point, there is limited scope to change the outcome. The team is left explaining a result rather than helping shape it.

The core issue is not that planning is missing. It is that planning is happening at the point of filing, when there is very little room left to adjust.

What a lighter, year-round Self Assessment model looks like

A more sustainable approach does not have to mean a new, complex advisory service. In practice, a lighter model of Self Assessment planning can be built around three ideas.

1. Move a small number of conversations earlier

Rather than trying to “fix January” in one go, it can be more effective to bring forward the conversations that have the biggest impact on the eventual tax bill and payments on account. That often means looking earlier at directors with variable dividends, clients whose income regularly crosses key thresholds, or individuals with multiple income sources such as salary, dividends and rental income. The aim is not to speak to every Self Assessment client more often. It is to speak to a selected group at a more useful time.

2. Attach planning to touchpoints that already exist

New meetings are hard to sustain. A more realistic approach is to attach a short planning segment to something you already do, such as adding a 15–20 minute personal tax check-in to year-end accounts sign-off, including a quick Self Assessment review in an existing quarterly catch-up, or using a scheduled call to confirm what has changed and what it might mean. This keeps planning inside the current workflow, rather than asking the team to find completely new slots in the diary.

3. Use a single, clear view to guide the discussion

Clients do not need a mini tax lecture. They need a clear picture of what their current position is likely to mean. A simple view that brings together expected income, projected tax and payments on account makes the conversation more concrete. It lets you say: “If things continue as they are, this is roughly what January will look like. If you change X or Y, here is how that could shift.” That is often enough to move a conversation from reactive to planned.

Making Self Assessment planning realistic for a busy team

Even if the logic is clear, a fair question comes up quickly:

“How do we make this work when the team is already busy?”

One way to approach this is to start narrow. Rather than introducing planning for every Self Assessment client at once, you can begin with a small, clearly defined group where the potential impact is high and the pattern is repeatable, such as directors whose drawings change regularly or individuals with several income streams.

It also helps to keep the format simple. Long questionnaires and complex documentation are hard to sustain. A short set of consistent questions around what has changed since last year, what is expected to change before the year-end, and what the client’s immediate priorities are is often enough to frame a useful conversation without adding much extra work.

Finally, the outcomes need to be easy to re-use in January. Capturing the result of the planning conversation in a format the team can pick up quickly at filing time, whether that is a short summary in the client’s file, a saved planning scenario for their Self Assessment, or clear notes on agreed actions, means the team is not starting again from a blank page when the deadline approaches.

A simple workflow you can adapt

Every firm will structure Self Assessment planning slightly differently, but one practical starting point could look like this:

- Identify a first group of clients

For example, directors with variable drawings, or clients whose income is close to higher rate bands. - Choose one earlier touchpoint

Attach a short personal tax review to accounts sign-off or an existing meeting, ahead of the 5 April year-end. - Define what you will cover

Agree a short agenda: what has changed, what the projected position looks like, and whether the client wants to adjust anything. - Capture the outcome in a consistent way

Record the key figures, the likely Self Assessment position and any agreed actions in a format your team can easily access later.

From there, you can refine the questions, expand to other client groups and involve more of the team once the approach feels proven.

Common questions about Self Assessment planning

Do we need a specialist tax team to offer Self Assessment planning?

Not necessarily. A light-touch approach to Self Assessment planning can be delivered by non-specialists, as long as they have clear parameters, a reliable way to run scenarios and a defined client group to focus on. A practical way to start is to work with a small number of directors or individuals whose income patterns change regularly, then build confidence from there.

Will Self Assessment planning add more work in January?

The aim is the opposite. Some of the work shifts earlier in the year, but the payoff is fewer surprises when returns are prepared. With at least one earlier touchpoint for selected clients, the January workload becomes more about confirming an agreed position than reacting to unexpected outcomes.

How can a small firm start with Self Assessment planning?

A straightforward starting point is to choose a narrow group of clients and add one short review before year-end. That review brings together key changes in income, shows what they are likely to mean for the next tax bill and payments on account, and gives the client a chance to adjust if they wish. The process can then be refined and expanded over time.

Do we need to brand this as a separate “advisory” service?

Not always. You can treat Self Assessment planning as an extension of the support you already provide to key clients and keep the language very simple. Alternatively, you can choose to package it as a defined personal tax planning service. The important part is the structure and timing of the conversations, not the label used.

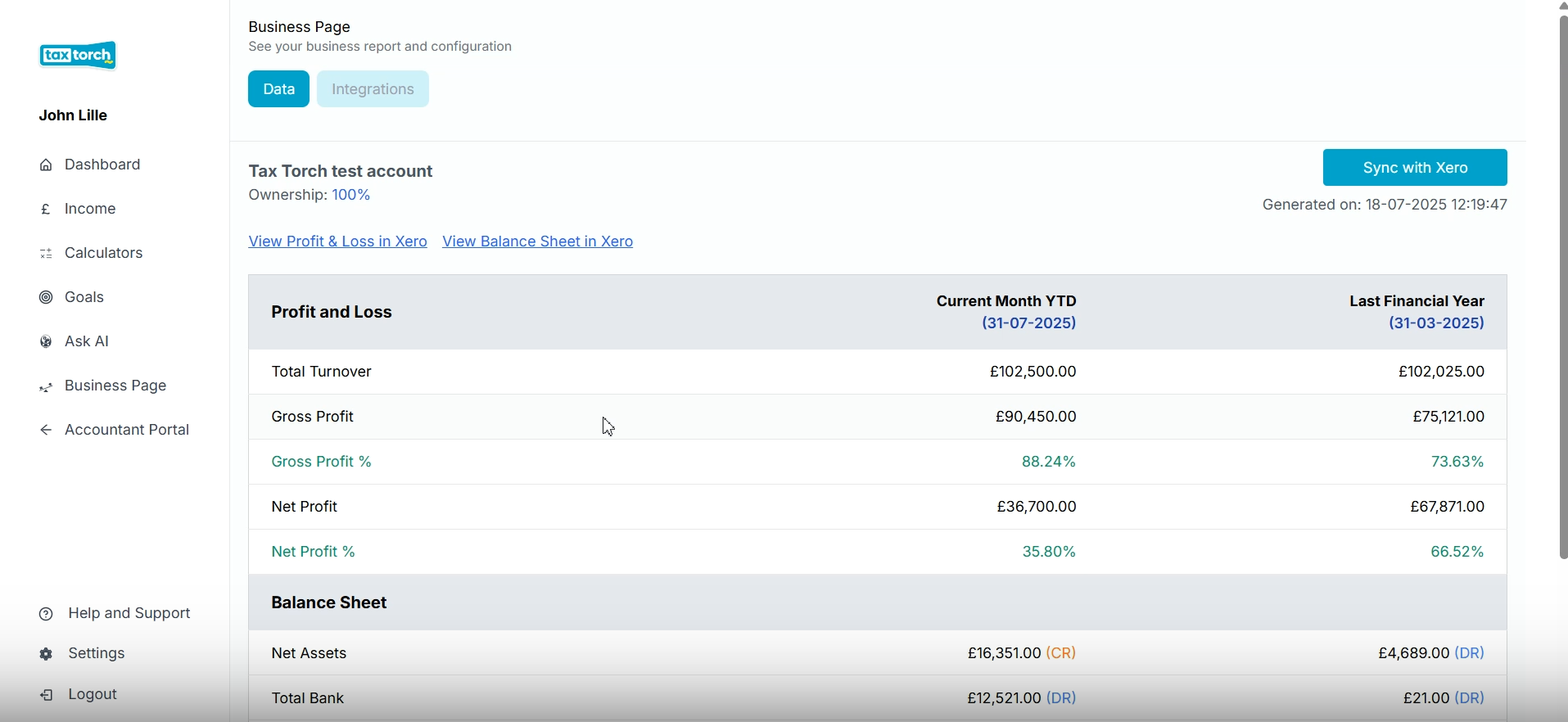

Where Tax Torch fits

Tax Torch is designed to support this kind of lighter, year-round Self Assessment planning without requiring a dedicated personal tax specialist in the team.

It gives your firm a way to:

- Bring key personal tax details for an individual into one place

- Run straightforward scenarios for salary, dividends, rental income and other common planning areas

- See how changes are likely to affect total tax due and payments on account

- Turn those outputs into clear explanations you can share with clients

Instead of adjusting spreadsheets each time something changes, your team can work from a planning view that reflects current rules and makes it easier to talk about what January might look like long before the deadline.

A small first step towards a calmer January

Self Assessment will always be a busy part of the year. The question is whether it has to push everything else aside.

You do not need a new service line or a full-scale transformation to change the experience for your team. A small, focused shift can make a real difference. Choosing a narrow group of clients, adding one short, structured review before year-end and using a clear view of their position to guide the conversation is often enough to change how January feels.

If you would like to see how this could work with your own clients, we can walk through a few example workflows and scenarios on a short demo.

.png)

.png)